Estimated read time: 8 minutes

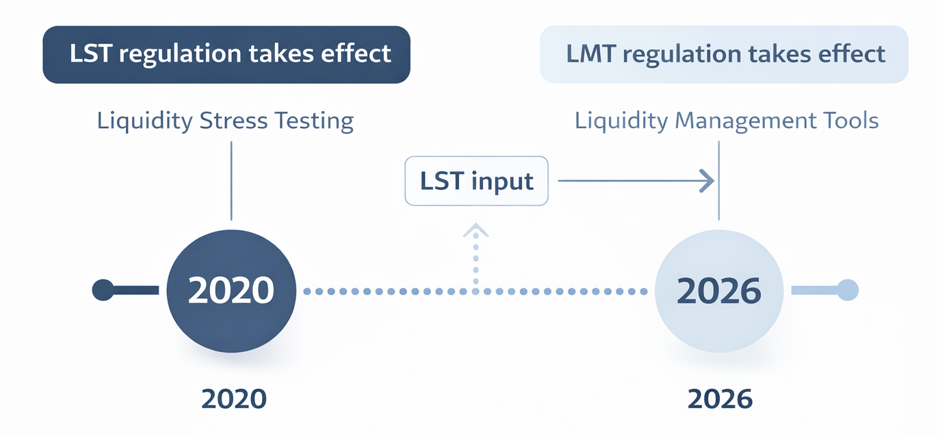

Liquidity Stress Testing (LST) has been a core regulatory requirement for asset managers since the introduction of the ESMA Guidelines in 2020. It plays a key role in assessing whether a fund can meet its obligations under both normal and stressed conditions.

With the introduction of new Liquidity Management Tool (LMT) regulations in April 2026, the importance of LST has increased significantly. These regulations explicitly rely on LST as an input for selecting and calibrating appropriate liquidity management tools.

As a result, LST is no longer just a standalone risk management exercise. It has become a critical component in demonstrating robust liquidity management under heightened regulatory scrutiny, requiring a structured, consistent and reproducible approach.

The importance of Liquidity Stress Testing

From a regulatory perspective, the purpose of LST is to ensure a consistent and harmonised approach to liquidity risk management across the European market. The ESMA guidelines aim to increase the standard, consistency and frequency of LST, ensuring that funds are assessed in a comparable and robust manner.

For asset managers, this translates into two key questions:

- How liquid is the fund under normal conditions?

- How does that liquidity change under stressed conditions?

Answering these questions requires a structured approach that considers the liquidity of the asset side, the behaviour of the liability side and the combined effect of both on the fund’s overall liquidity position.

LST is expected to produce clear, measurable indicators that provide a solid understanding of the fund’s liquidity risk, highlight potential vulnerabilities and define thresholds at which liquidity pressure may arise. These insights should directly support decision-making, for example by identifying when action is required, how liquidity can be improved or which liquidity management tools may need to be applied.

A practical starting point

A practical starting point for Liquidity Stress Testing is an assessment of the fund under normal conditions. This means understanding how the fund’s liquidity behaves in its current state, taking into account its key characteristics such as investment strategy, dealing frequency and structural constraints.

A comprehensive view of liquidity typically considers three core dimensions:

- Assets

The composition of the portfolio, concentration of positions and the inherent liquidity of underlying assets determine how easily the portfolio can be liquidated under normal market conditions. - Liabilities

The structure of the investor base, including concentration and type of investors, provides insight into potential redemption pressure and how liquidity risk may materialise. - Fund dynamics

Historical patterns in subscriptions and redemptions, as well as the development of NAV and units over time, provide context on what constitutes normal inflow and outflow behaviour.

Designing the LST framework

The initial assessment under normal conditions highlights where potential risks may arise, which in turn informs how LST should be applied. This includes identifying relevant risk factors across both the asset and liability side, determining which scenarios are meaningful and how severe they should be.

In practice, this means defining:

- The key liquidity risk drivers of the fund

- The types of scenarios to be applied and the assumptions underpinning them

- The outputs and indicators used to monitor liquidity risk over time

- How results are reported and embedded into decision-making across risk, portfolio management and senior management

LST is expected to produce actionable insights that support follow-up actions, whether that is adjusting the portfolio, setting internal limits or preparing for periods of stress.

These elements should be formalised within an LST policy as part of the broader risk management framework. This policy captures governance, roles and responsibilities, reporting and escalation procedures, as well as key modelling choices such as scenario design, assumptions, liquidation approaches and testing frequency.

The frequency of LST is not fixed, but should reflect the nature, scale and liquidity profile of the fund. While annual testing is a minimum requirement, more frequent testing—such as quarterly—is often appropriate.

Defining stress scenarios

Stress scenarios should be severe but plausible and reflect a range of conditions that may impact the fund’s liquidity. Rather than relying on a single perspective, LST should incorporate multiple types of scenarios that together cover the full balance sheet.

- Historical scenarios

Scenarios based on past market events, such as the global financial crisis or COVID-19, used to replicate how markets and investor behaviour evolved during those periods. - Hypothetical scenarios

Forward-looking scenarios reflecting potential risks, such as changes in macroeconomic conditions (e.g. interest rates or credit spreads) or idiosyncratic events affecting the fund, such as reputational issues or fraud. - Reverse stress testing

Scenarios constructed by identifying the conditions under which the fund would no longer be able to meet its obligations, and working backwards to determine what combination of events could lead to such an outcome.

Source: CBOE via FRED. Market volatility (VIX) over time, illustrating historical stress periods.

Each scenario is translated into a set of assumptions affecting both sides of the balance sheet. On the asset side, this may include changes in market conditions, trading volumes or pricing. On the liability side, it may involve shifts in investor behaviour, such as increased redemption activity or concentration effects.

This translation step is essential, as it determines how a scenario is applied within the stress testing framework. Assumptions should remain realistic and, where uncertainty exists, conservative. In particular, managers should avoid overly optimistic assumptions—for example, assuming that assets can be liquidated at full average daily volume without empirical support.

Stress testing the balance sheet

The defined scenarios are applied to the fund’s balance sheet to assess their impact on overall liquidity. This assessment considers both sides of the balance sheet individually, as well as their combined effect.

On the asset side, the focus lies on the ability to liquidate positions under both normal and stressed conditions. This typically includes:

- Time to liquidate positions under varying market conditions

- Liquidation cost, driven by asset type, trade size and execution horizon

- Feasibility of liquidation, taking into account investment policy, risk profile and investor interests

Market conditions play a key role in this context. Under stress, reduced liquidity, wider bid-ask spreads and increased volatility may significantly affect both the feasibility and cost of liquidation. Assumptions should therefore reflect realistic execution conditions and avoid overly optimistic expectations, particularly for less liquid assets where pricing and market depth may be limited.

On the liability side, the focus is on potential outflows and other obligations that may put pressure on liquidity. This includes:

- Redemptions, typically the primary driver of liquidity risk

- Investor structure, such as concentration and investor type

- Behavioural patterns, reflecting how investors may respond under different scenarios

In addition, other balance sheet obligations may become relevant depending on the fund’s structure. This includes, for example, margin calls on derivatives, committed capital requirements, obligations arising from securities financing transactions or changes in interest and credit conditions. These elements can materially impact available liquidity and should be reflected where appropriate.

The interaction between assets and liabilities is ultimately what determines liquidity risk. Reduced ability to liquidate assets combined with increased outflows or obligations can lead to liquidity pressure, particularly in stressed environments. A combined view of both sides of the balance sheet therefore provides the most complete picture of the fund’s resilience.

Towards a structured workflow approach

LST is a multi-step process that needs to be repeated periodically while maintaining consistency in methodology and assumptions. This makes it particularly well-suited for a structured workflow approach.

By embedding LST into such a workflow, managers can ensure automated updates based on current portfolio data and outputs that remain consistent, comparable and directly usable for decision-making.

At Amsshare, we embed the full LST process into a structured workflow, enabling managers to perform updates in seconds while maintaining full regulatory compliance and strengthening ongoing liquidity risk management.

You can read more here about how these workflows are developed.

Curious how to stay compliant without manual effort? Feel free to get in touch.